71 / 127

71 / 127

Barriers and Opportunities for Enhancing Capital Flows

In the COMCEC Member Countries

63

scores across all time periods for the pool of COMCEC Countries. Three BER categories –

foreign trade and exchange regime (shown here), market opportunities, and financing –

revealed the trend that higher BER scores related to higher levels of private capital flows.

Does economic size matter?

To explore whether the size of the economy is a factor in attracting capital flows, we

examined private capital flows in relation to GDP. As can be seen with the foreign trade and

exchange regime categories (shown here), there is a positive relationship when private

capital flows are viewed as a share of GDP.

Does an improving business environment induce growth in private capital flows?

The next step was to seek evidence that a changing business environment attracts capital

flows. In the data analysis we tracked the change in a BER category and the change in capital

flows. The financing category (see right), shows a moderately positive relationship, implying

that an improving financial environment induces capital flows. The picture was less clear,

however, for the other BER categories.

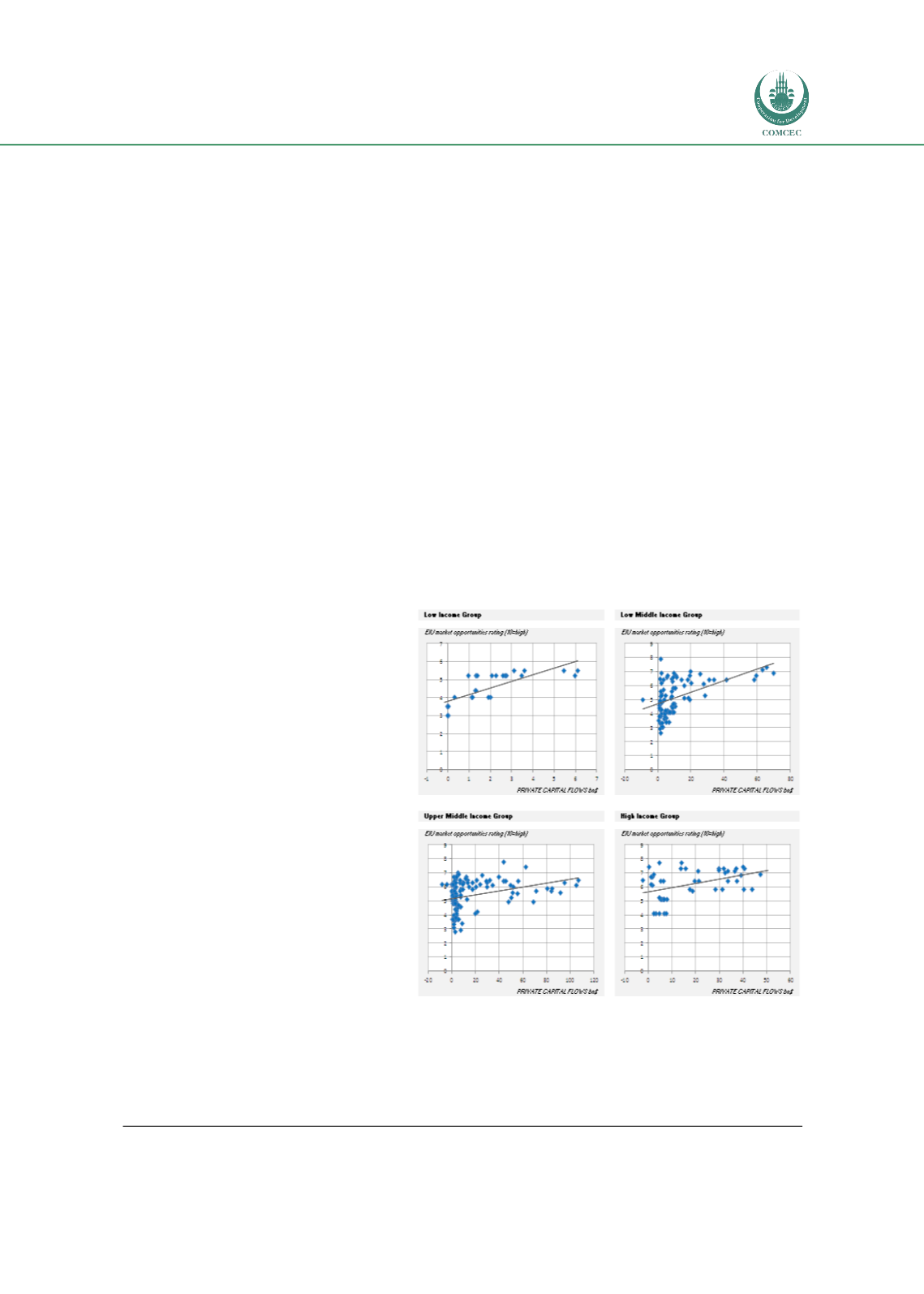

Does the apparent effect of the business environment depend on the level of income?

The EIU conducted further analysis

on the basis of the World Bank’s four

income categories – low-income,

lower-middle income, upper-middle

income, and high income. This

enabled analysis of the influence of

the business environment for high

and low income countries. The three

BER categories – foreign trade and

exchange

regime,

market

opportunities, and financing – were

more relevant for lower income

countries.

The

macroeconomic

environment and policy towards

foreign investment showed no such

pattern across income groups.

Caveats

The data analysis discussed here is

preliminary in nature and does not allow firm conclusions to be drawn about the causality

of the BER scores examined here. While this analysis can point towards potential

relationships, a more sophisticated regression analysis would need to be undertaken to be

able to make more conclusive statements about the causal link between BER scores and

private capital flows.