99 / 182

99 / 182

Improving the Role of Eximbanks/ECAs in the OIC Member States

91

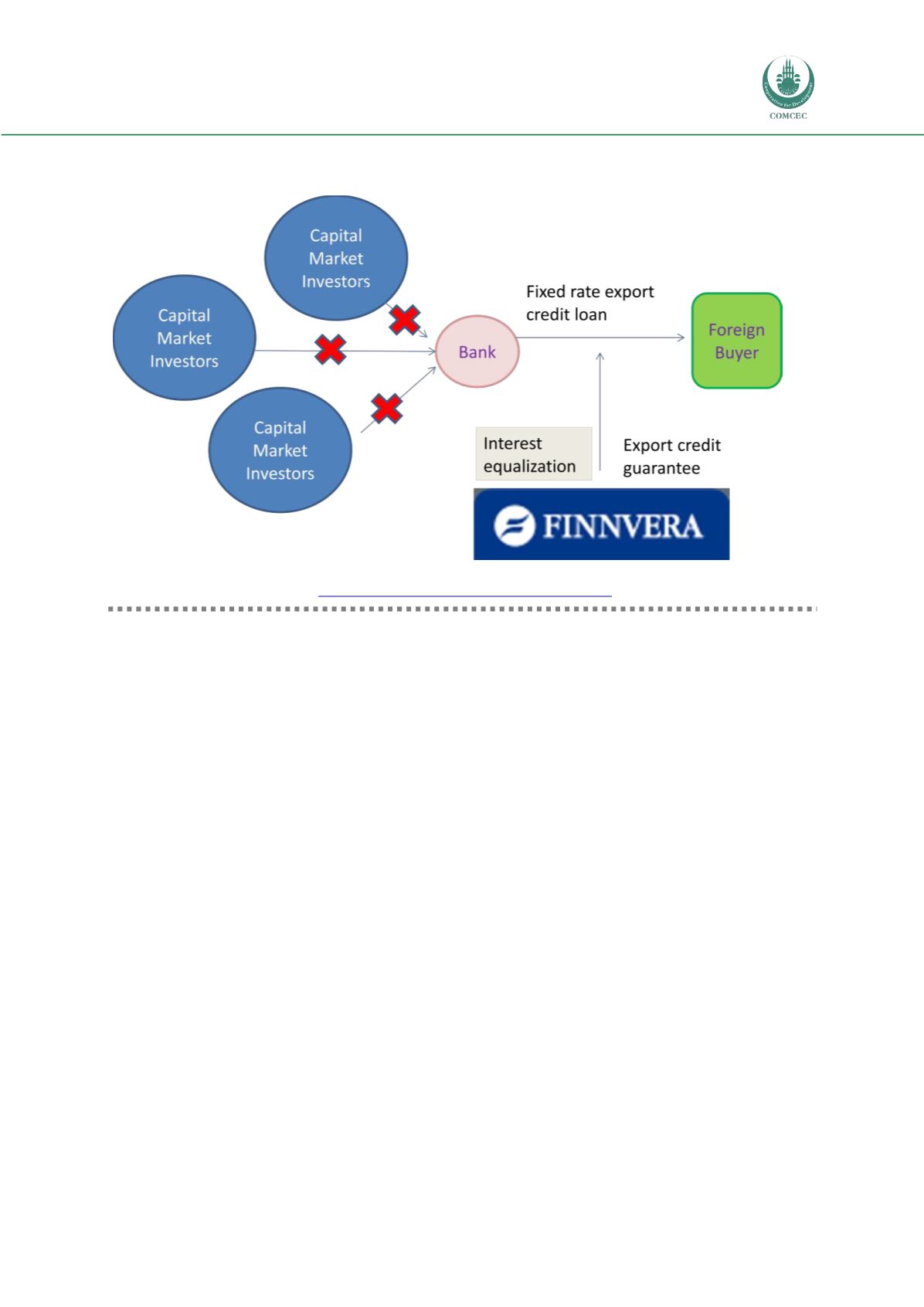

Figure 7: Market Disruption during the global finance crisis in 2008-2009

Source: Evaluation of Finnvera Plc

( www.tem.fi/files/33486/TEMjul_28_2012_web.pdf )The temporary funding scheme which was introduced in 2009 and a more permanent scheme

was put in place using FEC which then refinances commercial banks and offloads the asset into

the capital markets using securitizations.

There is no doubt about the effectiveness of Finnvera and its ability to identify and meet the

demands of the market, particularly during the Global Financial Crisis. Finnvera’s business

activities – focusing mostly on large capital goods exports and working capital for shipbuilding –

have little in common with OIC ECAs. However, its analytical approach can be applied in any

context and as a result, there are some useful lessons to be drawn from the Finnish example.

1.

Understand not only the nature of the market gap but why it is there:

there could be

a myriad of reasons why banks do not lend; they could be uncomfortable with the

borrowers’ creditworthiness, they could have reached internal risk limits on certain

types of risks, they might have sufficient exposure in a particular sector. Or, as was

happening in Finland and the rest of Europe during the global financial crisis, banks

simply could not borrow to lend. Finnvera understood the problem and developed a

solution that specifically addresses the need.

2.

Price to risk, but consider exporter competitiveness:

understanding the impact of

pricing on exporters balanced against an ECA’s own risks and costs is a critically

important function. Trade-offs need to be made.