84 / 231

84 / 231

Diversification of Islamic Financial Instruments

70

An important challenge for the Islamic banking industry in Pakistan is that it is commonly

perceived as less profitable (for depositors) than the conventional banks. This is partially

because of the limitation of Shariah-compliant investment avenues open to Islamic banks. In

December 2016, the liquid assets of Islamic banking institutions rose to PKR 610 billion

(approx. USD 5.8 billion), compared to PKR 566 billion in December 2015

52

It is said that

Islamic banks are not treated at a level playing field with the competing conventional banks.

The table below (Profit Rates for Islamic banks) describes the comparative profit rates offered

by the main (full-fledged) Islamic banks in Pakistan, on their Mudarabah-based deposit savings

accounts. As it is illustrated, the rates are comparatively lower than those offered by

conventional banks. The difference is often attributed to the less Shariah compliant investment

avenues available to Islamic banks, and the fact that Islamic banks in Pakistan often do not

have a level playing field given the regulations, available Shariah compliant government

securities and liquidity management options.

Islamic banks, like their conventional counterparts are faced with the challenge of having

short-term liabilities (in terms of deposit accounts that can be called at any time) with medium

to long term assets on their balance sheets. Typically, Islamic banks offer several Mudarabah-

based deposit instruments to their customers, with their profit rates varying by as much as

two or three times

53

. Though the profit-sharing ratio is kept constant, varying rates are offered

by the difference in weightages, and gives depositors financial incentive to deposit larger

amounts of money, keep them fixed for longer periods of time, or receive profit payments at

lesser frequency (e.g. quarterly, yearly or at maturity, instead of monthly).

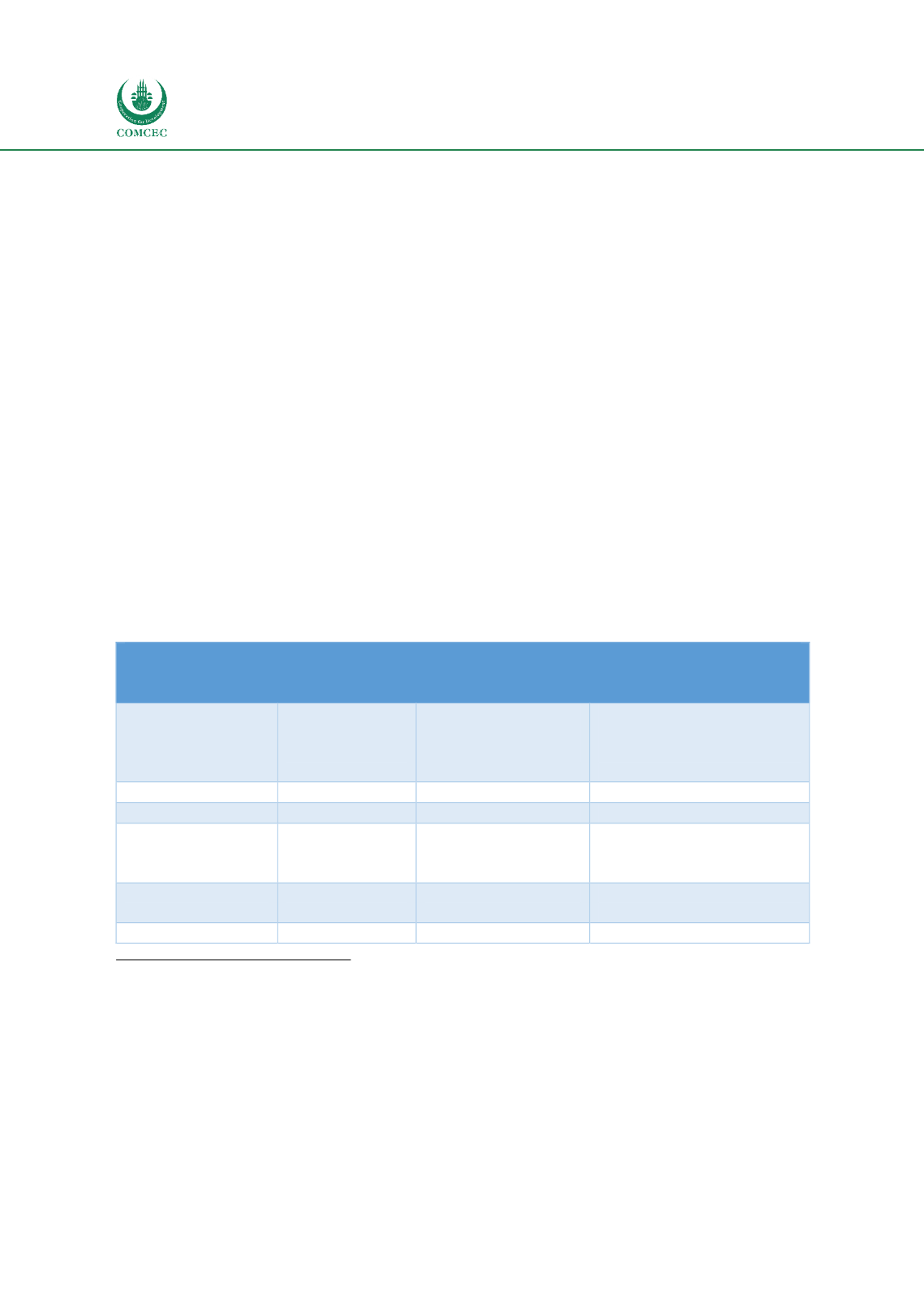

Table 30. Profit Rates of Islamic vs. Conventional Bank in Pakistan

Mudarabah-based deposits and their comparative profit rates, in PKR, offered by

Islamic banks in Pakistan – as at March 2017

Islamic Bank

Basic savings

account profit

rate

(annualized)

Range of rates on

different saving

account instruments

Mudarabah profit-loss

sharing ratio used (PSR)

Rab-ul-Maal/depositor:

Mudarib (bank)

Meezan Bank Ltd

2.40%

54

2.40 – 5.98%

55

50% – 50%

56

Bank Islami

2.60%

2.60 – 5.90%

50% - 50%

Dubai Islamic

Bank Pakistan

(DIBPAK)

1.78%

1.73 – 5.18%

50% - 50%

Bank AlBaraka

Pakistan

2.45%

2.45 – 6.40%

60% - 40% (Depositor:

60%)

MCB Islamic Bank

2.31%

2.25 – 6.03%

50% - 50%

52

State Bank of Pakistan Islamic Banking Bulletin, December 2016.

53

This is a State Bank of Pakistan regulation for Islamic banks: the maximum deposit rate offered cannot exceed more than

three times the minimum rate offered.

54 The Mudarabah-based saving account is inherently a one month Mudarabah between the depositor and Islamic bank. The

profit rates are declared at the end of every month, and weightages and PSR at the start of each month. The profit rate for

the simplest saving account is quoted here.

55

These ranges exist because different weightages are assigned to different types of saving account instruments, based on

amount, payment frequency (monthly, quarterly, yearly), term deposits and tenure. The highest profit rate is typically for a

five or seven year fixed term deposit instrument

56

Profit sharing ratios (PSR) have been taken as at 31

st

March 2017 from the respective websites of the five full-fledged

Islamic banks in Pakistan. The PSR is found in ‘Weightages’ section, which are updated at the start of every month.