74 / 231

74 / 231

Diversification of Islamic Financial Instruments

60

Sukuk structure due to some reasons such as the requirement for underlying assets is

relatively varied which can be real assets, project based asset or services. In addition, the

Sukuk that is structured using

ijarah

or

mudarabah

contract can be traded in secondary

market and hence preferred by investors.

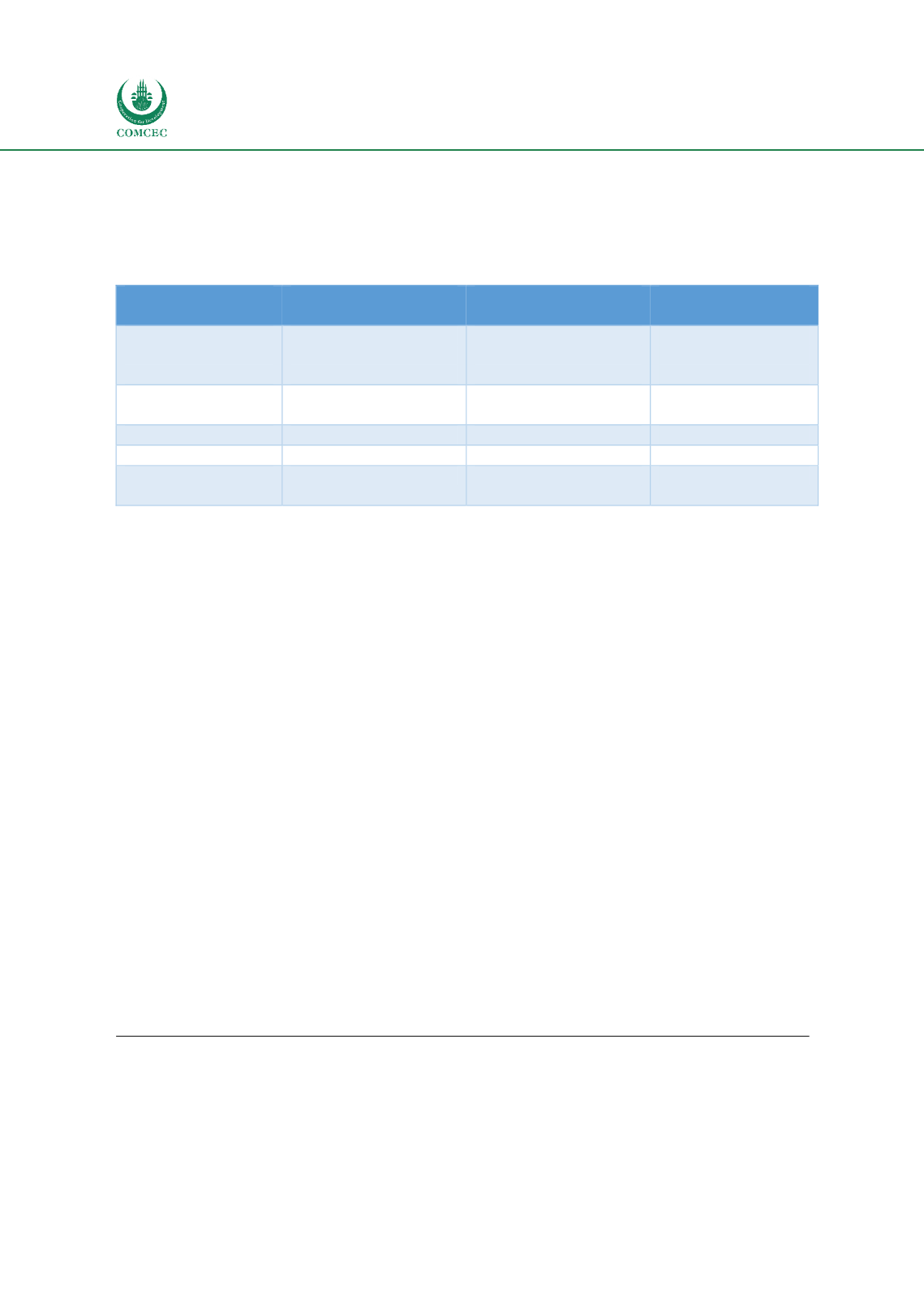

Table 27: Structure of Indonesian Sovereign Sukuk (SBSN/Surat Berharga Syariah Nasional)

Ijarah Sale and Lease

Back

Ijarah al-Khadamat

Ijarah Asset to be

Leased

Classification on

AAOIFI Shariah

Standards 17

Certificates of

ownership in leased

assets (3/1)

Certificates of

ownership of described

future services (3/2/4)

Certificates of

ownership of assets

to be leased (3/1)

Underlying Asset

State-Owned Assets

Hajj Services

Infrastructure

Projects

Coupon

Fixed rate

Fixed rate

Fixed rate

Tradability

Tradable

Non- Tradable

Tradable

Series of Sovereign

Sukuk

IFR, SNI, SR, SPN-S

SDHI

PBS, SR

Source: Indonesia Stock Exchange 2016

The Sukuk market in Indonesia is dominated by sovereign Sukuk. The corporate sector seems

to have little interest in the issue of Sukuk, perhaps due to the complexities in Sukuk issuance

and their risk preferences. There are two main factors that are possibly contributing to this

phenomenon, namely the limitation in liquidity as secondary market is not that developed in

Indonesian capital market, and the behaviour of investors that prefer to hold the Sukuk to

maturity (especially the long-term investor such as Takaful companies, pension funds, and

others).

This phenomenon should be noted by the Indonesian authority in Islamic capital market, to

solve the problem of liquidity and secondary market trading to attract the corporate sectors to

issue Sukuk and hence the supply of the Sukuk in the market can be increasing.

It seems that in doing diversification of Shariah contracts (‘

aqd

), the Sukuk issuers are very

concerned with the preference of the investors. So far, Sukuk based on

Ijarah

and

Mudarabah

are preferred by Indonesian investors. Nevertheless, moving forward various types of

contracts based on

Murabahah

,

Salam, Istisna’, Musharakah, Wakalah bi al-Istihmar

, and others

can be used in structuring Sukuk as in other jurisdictions to attract investors (including

international investors) without relying too much on

Ijarah

or

Mudarabah

as in the present

scenario

.

In addition, the

Sukuk

structure such as in the form of perpetual Sukuk, exchangeable

and convertible Sukuk which can be found in other jurisdictions, are also not common in

Indonesian Islamic capital market. Those structures could be considered to diversify

Indonesian Sukuk market.

40

Ijarah Al-Khadamat

is a contract used in Sukuk using services as underlying asset. In this case, the underlying asset is Hajj

services. In this regard, Sukuk is categorized as certificates of ownership of describe future services as can be referred to

AAOIFI Sharia Standards Nomor 17 (3/2/4).

41

Ijarah Asset to be Leased

(

ijarah Milkiyyah al-Maujudat Al-Mau’ud Bisti’jariha)

is defined as a contract whereby the ijarah

object has been specified and some of its objects are already in existence when the contract is signed, but the delivery of

total ijarah object will be done in the future as agreed as can be referred to AAOIFI Scxhariah Standards Nomor 17 (3/1).