73 / 231

73 / 231

Diversification of Islamic Financial Insturments

59

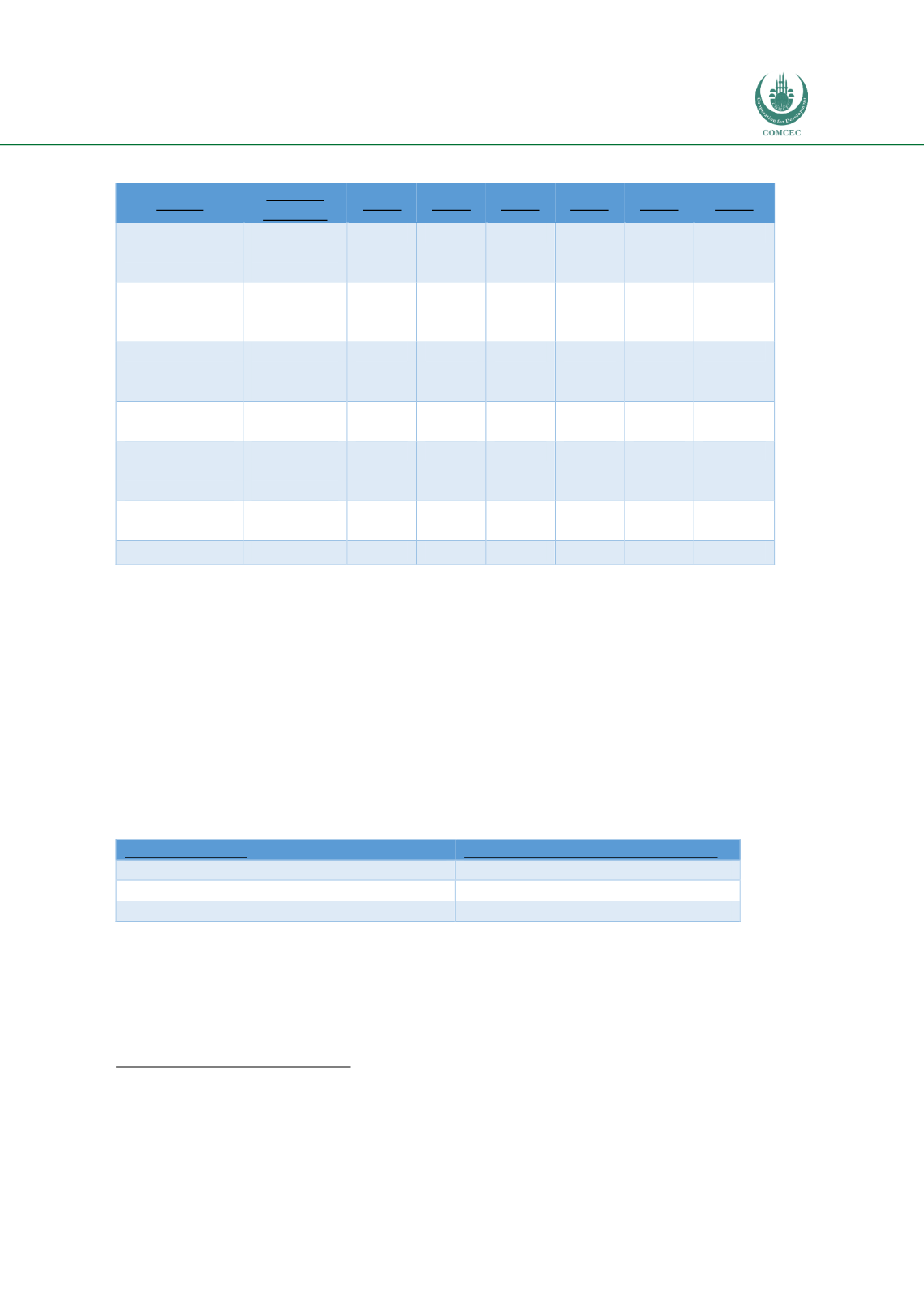

Table 25: Sovereign Sukuk Issuance (IDR Billion)

38

Sukuk

Shariah

Contract

2009

2010

2011

2012

2013

2014

Islamic Fixed

Rate Sukuk

(IFR)

Ijarah Sale

and Lease

Back

5,976

12,126 16,736 17,136 16,586 16,586

Ritel Sukuk

(SR)

Ijarah Sale

and Lease

Back

5,556

13,590 20,931 28,989 35,924 47,906

Indonesian

Sovereign

Sukuk (SNI)

Ijarah Sale

and Lease

Back

6,110

5,844

14,962 25,466 50,584 40,470

Hajj Fund

Sukuk (SDHI)

Ijarah al-

khadamat

2,686

12.783 23,783 35,783 31,533 35,533

Islamic

Treasury Bill

(SPN-S)

Ijarah Sale

and Lease

Back

1,320

195

8,633

5,165

Project Based

Sukuk (PBS)

Ijarah Asset

to be Leased

16.714 26,030 30,181

Total

20,328 44.344 77.733 124.28 169,29 175,842

Source: Indonesian Ministry of Finance (2016)

Financial Instruments Commonly Used

The National Shariah Board of Indonesian Ulama Council (DSN-MUI) has issued fatwa No.

32/DSN-MUI/IX/2002 on the permissible Sukuk contracts in Indonesia namely

Mudarabah

,

Murabahah

,

Musharakah

,

Salam

,

Istisna’

and Ijarah. However, the most common structures

used in Indonesian Sukuk structure are

Ijarah

and

Mudarabah.

The Corporate Sukuk in Indonesia are mainly structured following the principles of

Ijarah

and

Mudarabah

. At end-2015, corporate Sukuk based on an

ijarah

contract accounted for 65.9% of

total corporate Sukuk outstanding.

Table 26: Corporate Sukuk Instruments in Indonesia

Sukuk Structure

Outstanding Amount (IDR billion)

Sukuk Ijarah

4,974

Sukuk Mudarabah

1,079

Sukuk Mudarabah Subordinated

1,500

Source: Indonesia Stock Exchange 2016

Likewise, sovereign Sukuk in Indonesia are mainly structured using

Ijarah

contract. In

sovereign Sukuk, at least three types of

Ijarah

are used in the structure, namely

Ijarah

sale and

lease back,

39

Ijarah al-Khadamat

40

and

Ijarah

asset to be leased

41

. The preference to use

ijarah

in

38

Availabe at

http://dmo.aqilpapa.com/stats/statistik-sukuk/39

Ijarah sale and lease back

is defined as a contract whereby the buyer of an asset lease back of the asset that has been

bought to the seller. The underlying asset is usually land or building. This type of Sukuk is categorized as certificate of

ownweship of leased asset as can be referred to AAOIFI Shariah Standards Nomor 17 (3/1).