77 / 176

77 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

60

A significant fraction of OIC countries does not have an explicit deposit insurance

scheme, which should be improved to achieve a banking system which is immune to

bank panics and systemic banking crisis.

Most OIC countries do not engage in derivative trading activities and work with

relatively low leverage levels. Expansion of the banking sector towards these areas

might create problems, thus regulations of Basel III should be applied and monitored

closely.

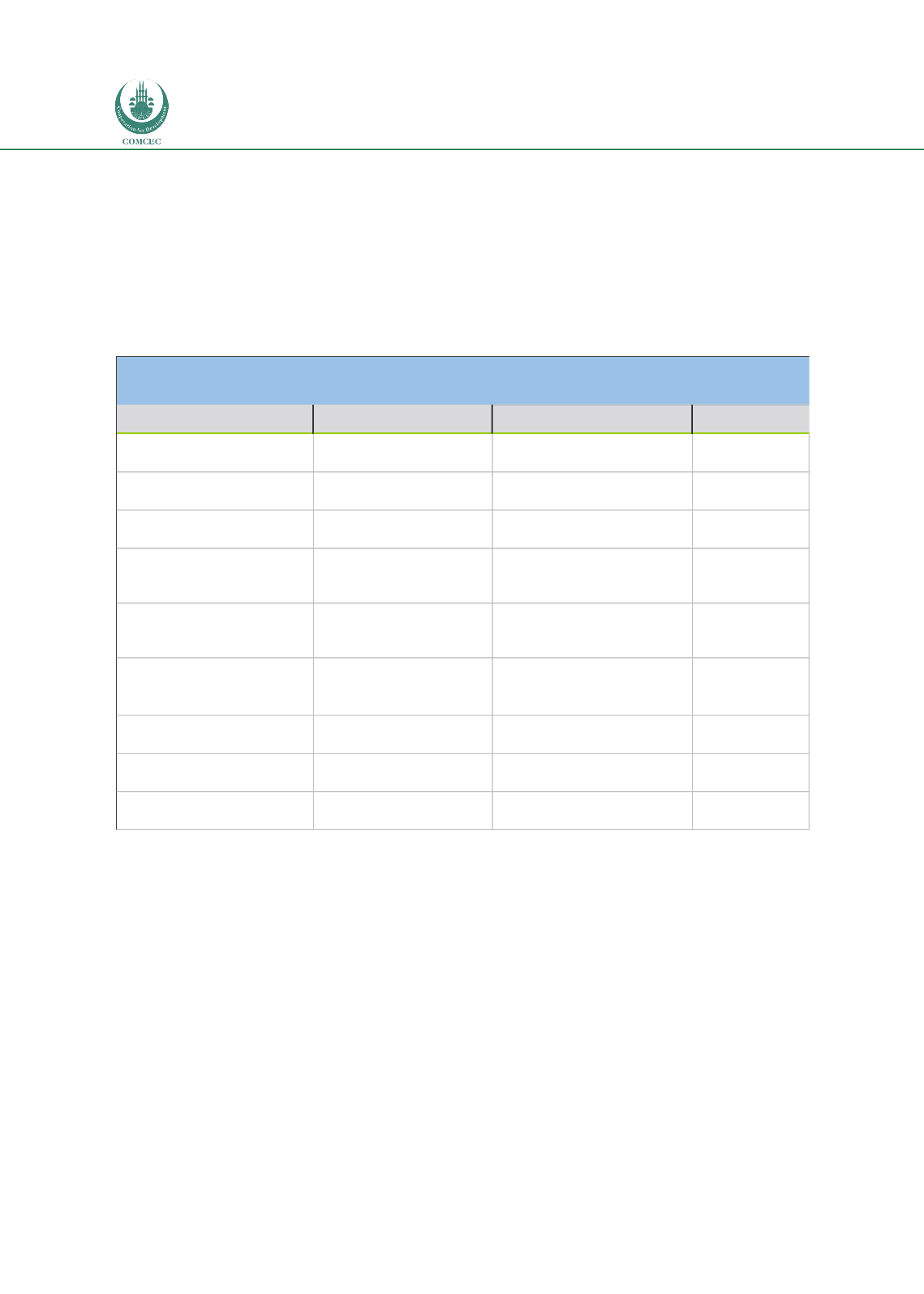

Table 26: SWOT Analysis – OIC Countries

Source: World Bank, Bank Regulation and Supervision Survey

Strengths, Weaknesses and Threats Analysis

Supervision Criteria

Strengths

Weaknesses

Threats

Scope of Banking Activities

Strong restrictions on permissible activities.

No major weaknesses

Financial deepening may

change the current structure.

Ownership Restrictions

Strong restrictions on ownership structure for

banks.

No major weaknesses

Capital Regulations

Stong capital regulations beyond the levels of

EU-27 and US.

Limited coverage of capital requirements on market

and operational risk.

Changes in BASEL III.

Supervisory Power

Most OIC countries have autonomous

supervisory authority for banking regulation.

In most OIC countries supervisory authority also

regulates financial sector. Supervisory power decline

in the aftermath of the 2008 crisis.

Structure of Supervision

Supervisory experience is equal to EU-27 level

slightly lower than US. Independence index

equal to EU-27 and US. Internaitonal standards

In most OIC countries supervisory authority also

regulates financial sector.

Private Monitoring

Stronger than EU-27 and US. Most OIC

supervision authorities use certified external

auditers.

No major weaknesses

External Governance

Equlally strong to EU-27 and US.

No major weaknesses

Restrictions on Entry into Banking Sector

Strong entry restrictions and licencing criteria.

No major weaknesses

Deposit Insurance

Fraction of OIC countries with explicit deposit

insurance schemes is still low.