109 / 176

109 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

92

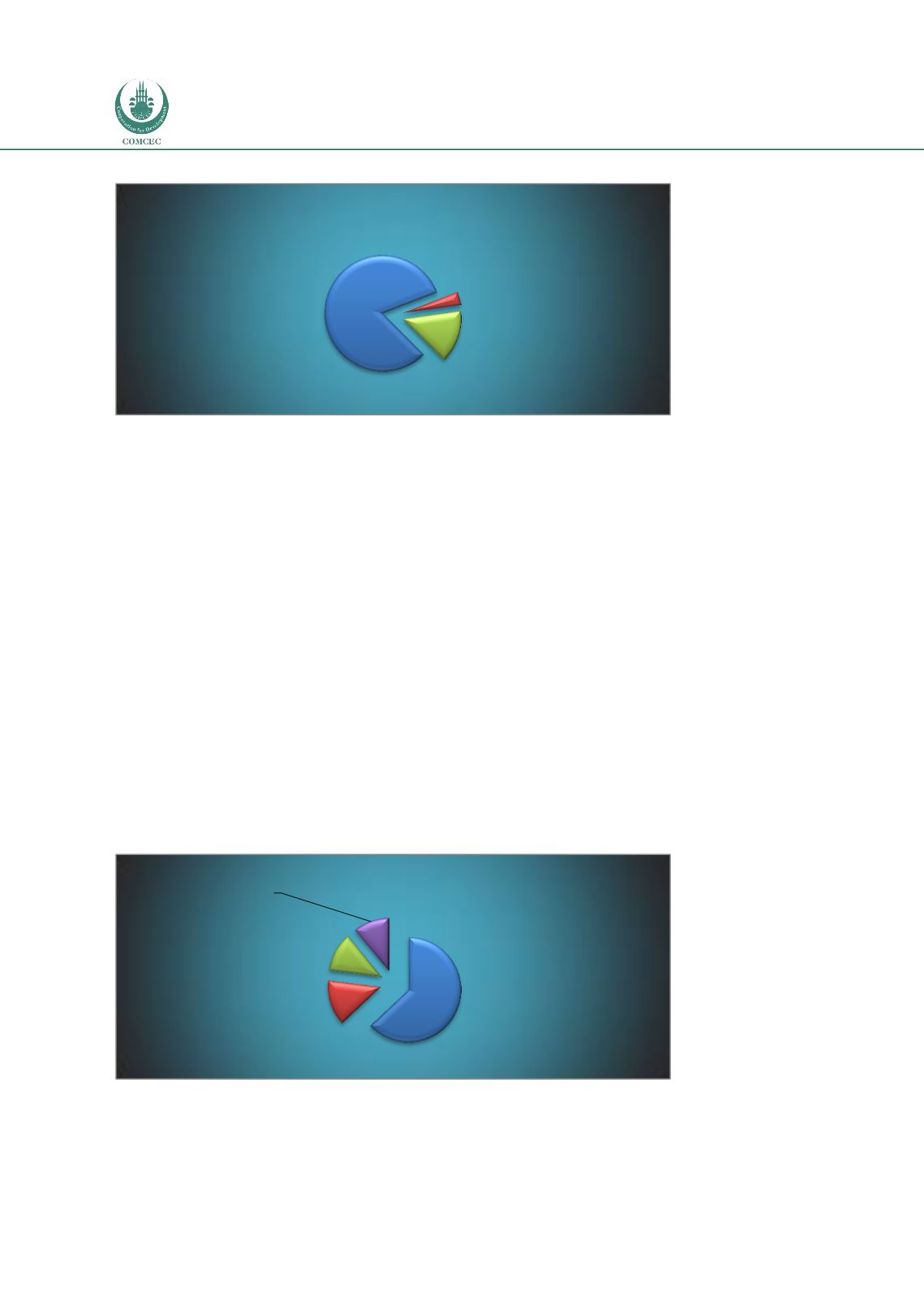

Figure 56: Liability Decomposition, Malaysia

Source: Bankscope

More than 80% of the liability in the Malaysian banking sector consist of customer deposits.

This is a very healthy statistics since this would imply the core liabilities in Malaysian banking

sector is in the form of deposits. This implies that loan/deposit ratio is around 75% as of 2013.

In terms of banking risk this number is rather tolerable. Many researchers claim that

loan/deposit ratio is one of important financial stability criteria. There is no clear benchmark

for this statistics but a ratio more than 120% to 150% may indicate some macro risk in that

economy.

As a conclusion, from the analysis and data above, Malaysian banking sector in general does

indicate a banking risk under normal economic conditions. However, a macro shock through

FED's interest rate hike and decrease in the global liquidity might have negative impact on the

Malaysian economy and banking sector. Therefore, macroprudential regulations might be

useful to tackle such episodes.

o

United Arab Emirates

In terms of asset decomposition of UAE we see similar picture to Malaysian banking sector.

Majority of UAE's assets are in the form of loans (63%).

Banking Sector

Figure 57: Total Asset Decomposition, United Arab Emirates

Source: Bankscope

Similar to the most OIC member countries, majority of the banking risk originates from credit

risk (92%), while operational risk is slightly lower than OIC average which is mainly due to the

Total Customer

Deposits

82%

Deposits from

Banks

3%

Total Equity

15%

Liability Decomposition

Loans

63%

Others

14%

Total Securities

12%

Cash & Due

From Banks

11%

Total Assest Decomposition