102 / 176

102 / 176

Improving Banking Supervisory Mechanisms

In the OIC Member Countries

85

(8). Conclusion

Banks in OIC countries did not feel the big repercussions of the recent financial crisis. This may

be related to various factors, including the relatively smaller size of the banking sector in these

countries relative to US and Europe. However, the banking sectors of these countries are

growing rapidly, and the global environment is becoming more challenging. Therefore,

countries in this region need to be ready for a different banking practice. Basel III

requirements will change banking practices both quantitatively and qualitatively. Loan

portfolios of almost all OIC countries have grown since the global credit crisis. This requires an

additional supervisory effort on credit risk measurement and management. Local credit rating

and loss given default calculations will become important for OIC countries. Since the

properties of each of these countries differ from Europe and the US, a different credit rating

data and methodology might be necessary. One suggestion would be to establish national

rating companies similar to the Turkish experience. In addition, until 2018 more capital and

liquidity is required in global banking. Until this period, capital adequacy ratios and liquidity

provisions will be calculated differently. These changes require a collaborated effort among

member states. Since these changes require different experience and expertise, a know-how

transfer among member states will be extremely beneficial for the whole OIC community. To

deal with financial stability issues in OIC countries, the establishment of an Islamic Financial

Stability Board could be an alternative to discuss. Since banking and financial problems in OIC

countries are different, exchanging available know-how within the Islamic countries can

enhance banking supervision. In addition, COMCEC's strategy document in 2012, clearly states

that member countries need to improve quality of regulation, supervision and cooperation

among its supervisory bodies.

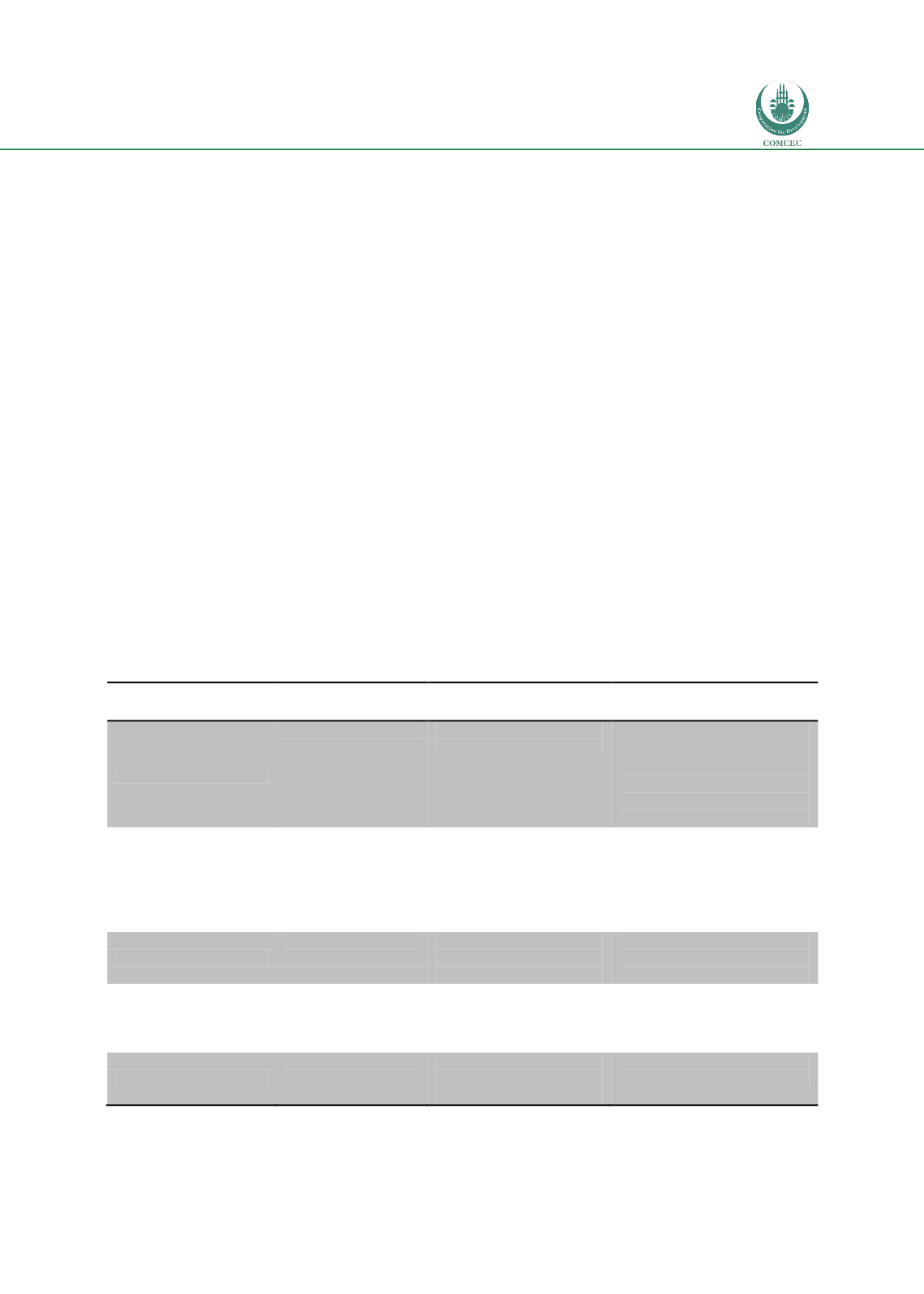

Table 40: Summary: What are the weak and strong points of banking supervision in OIC

Countries

Current level

Remarks

What can supervisors do to

measure the true risk?

Credit Risk

Relatively high

There is high capital

buffer

Standard measures can

understate the actual risks

Credit Rating methodology is

necessary.

Informality and lack of good

quality data is a challenge.

Market Risk

Relatively less

Accounting treatment of

securities is critical.

Trading book is very

small. So MR can be

underestimated.

Risk sensitive measures such

as VaR, ES should be

accompanied with standard

risk measures.

Stress VaR needs to be

estimated

Operational Risk

Higher than market

risk

As banking sectors are

growing Op. Risk could

grow

Op.Risk Data should be

collected for advanced

measurement

Interest Rate Risk

Potentially high but

data on maturity of

assets and liabilities

is hard to find.

As balance sheets are

growing it should be

watched

Asset and liability durations

of each banks can be

calculated

Liquidity Risk

Relatively better

than EU and US

banking

Could be important as a

supplementary tool for

stress testing

Useful to make a QIS on LCR

and NFSR