53 / 187

53 / 187

Islamic Fund Management

39

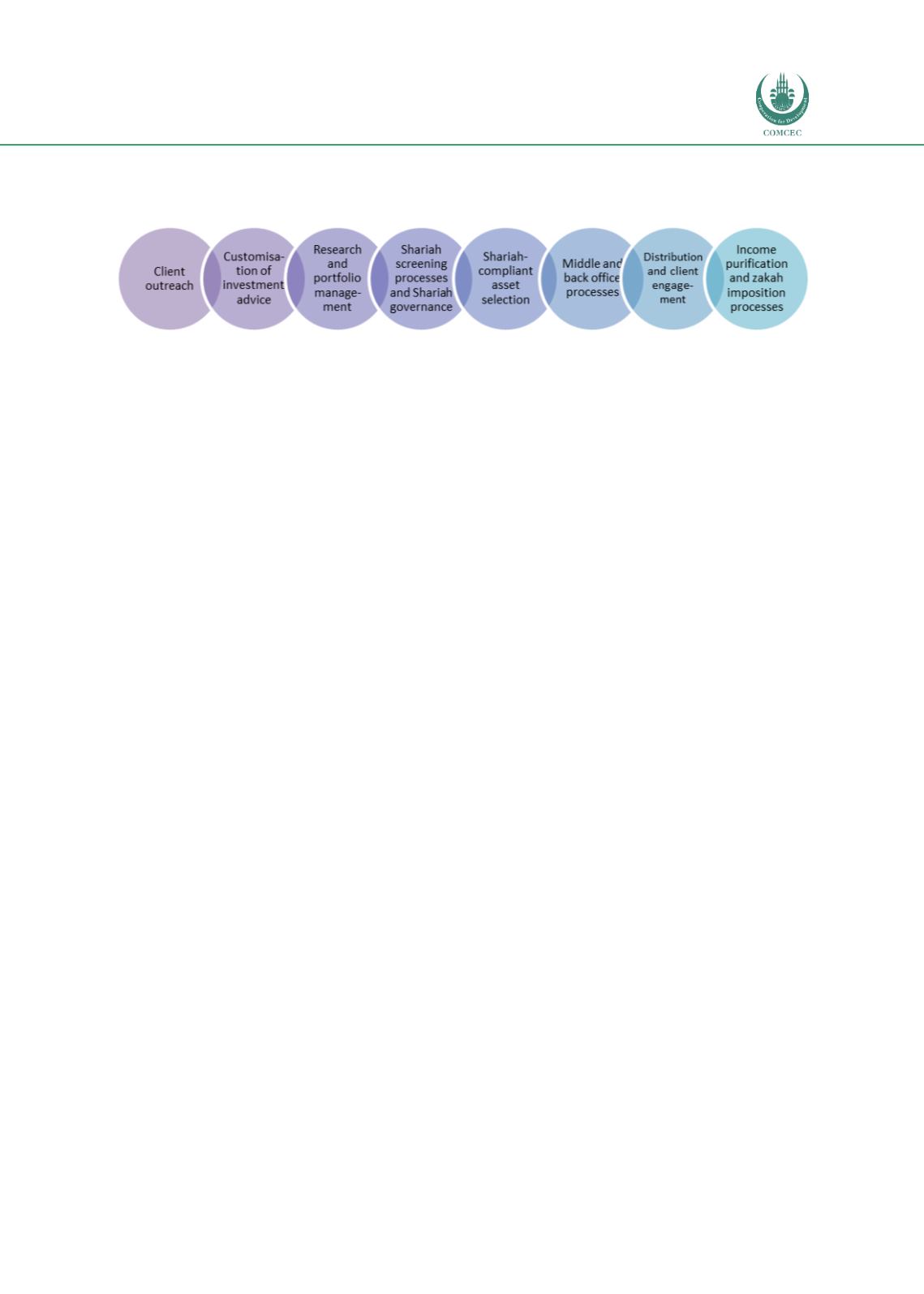

Figure 2.11: Quantum Change across the Value Chain of Islamic Fund Management

Source: Adapted from PWC (2017b)

For instance, fintech has already started changing investment advisory services by introducing

robo-advisers that take over the roles of human financial advisers, planners and fund

managers (Investopedia). The first robo-adviser was launched in 2008, known as ‘Betterment’.

The robo app or web platform allows clients to provide details on their financial situations and

investment objectives; the robo-adviser utilises the data to recommend an optimal portfolio to

them for a minimal fee. The service is much cheaper compared to the fees charged by

traditional advisers; it is an option available to clients who are comfortable with investment

products. Besides being low-cost alternatives, automated investment-management advice also

offers the advantages of being accessible to everyone, including low-budget investors, being

convenient and efficient, and being available 24/7.

The digital platform technology used is said to be similar to the automated portfolio-allocation

software used by human wealth managers, to passively manage investors’ portfolios since the

early 2000s. The difference with the robo-adviser is that the technology is now made

accessible to clients directly and can perform more sophisticated tasks such as tax-loss

harvesting (i.e. selling a security at a loss to offset a capital gains tax liability), investment

selection, retirement planning and overall financial advice.

The number of such robo-advisers has grown to about 200 in the US, with more being

launched by asset management firms every year (Investopedia). For the Islamic fund

management industry, they can be used to assist in the process of Shariah screening of

investments, Shariah-compliant asset selection, purification of investments and adding

transparency to the Shariah governance framework.