30 / 231

30 / 231

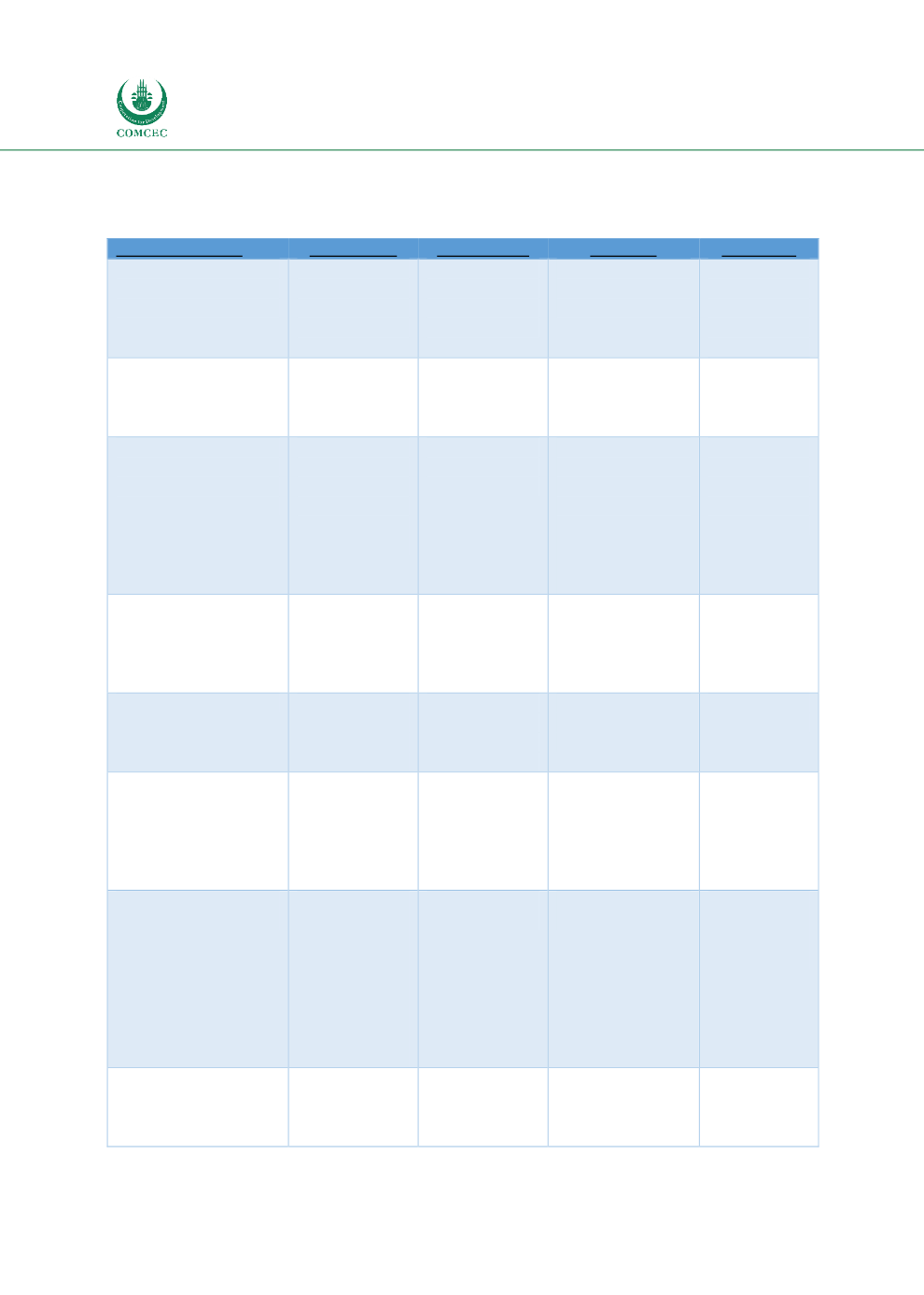

Diversification of Islamic Financial Instruments

16

Different Deposit Products Trade Finance and Treasury products in Middle East North

Africa Malaysia and Indonesia

Table 7: Deposits

Product/Process

Middle East

North Africa

Malaysia

Indonesia

Savings Account

Based on : Wadiah

Mudarabah, Qard

Mudharabah

and Qard are

standard

offerings

Mudharabah

and Qard are

standard

offerings

Wadiah is more

popular than

Mudharabah

Mudharabah

is most

popular,

followed by

Wadiah

Current Account

based on: Wadiah

Mudharabah Qard

Qard and

Mudharabah

are standard

offerings

Qard and

Mudharabah

are standard

offerings

Only Wadiah is

offered to

customers

Only Wadiah

is offered to

customers

Fixed Deposit based

on: Mudharabah,

Commodity

Murabahah Wakala

All three are

popular

products,

especially

within GCC

countries

All three are

popular

products

Mudharabah is the

standard offering.

Commodity

Murabahah and

Wakala are

gradually

becoming more

popular

Only

Mudharabah

is being

offered to

customers

Recurring

Deposits/Saving Plan

to increase deposits

Popular scheme

offered to

customers as a

“forced saving

plan”

Popular scheme Slow take-up as

Takaful unit-linked

plan is more

attractive to

customers

Popular

scheme to

encourage

saving for Hajj

and Education

Structured Products

Products are

offered to

selected

customers

Products are

offered to

selected

customers

Products are

offered to selected

customers

Not offered to

public yet

Profit Distribution

Adopt guideline

issued by

AAOIFI on

Mudharabah-

based products

Adopt guideline

issued by

AAOIFI on

Mudharabah-

based products

Adopt guideline

issued by AAOIFI

but more refined

and complex

Revenue-

based

(instead of

profit based)

but less

complex

Liquidity

Management

Standard

offering when

banks promote

their cash

management

services to

commercial and

corporate

customers

Emerging

requirements

Same as ME and

Africa

Emerging

requirements

in Indonesian

market

Fund Management

(Allowing banks to

create multiple funds

or pools meant for

Very popular

arrangement

wherein

customers can

Popular

arrangement

wherein

customers can

Low demand from

customers.

However, non-

bank financial

Emerging

requirements

but take up

from