45 / 227

45 / 227

Improving Public Debt Management

In the OIC Member Countries

31

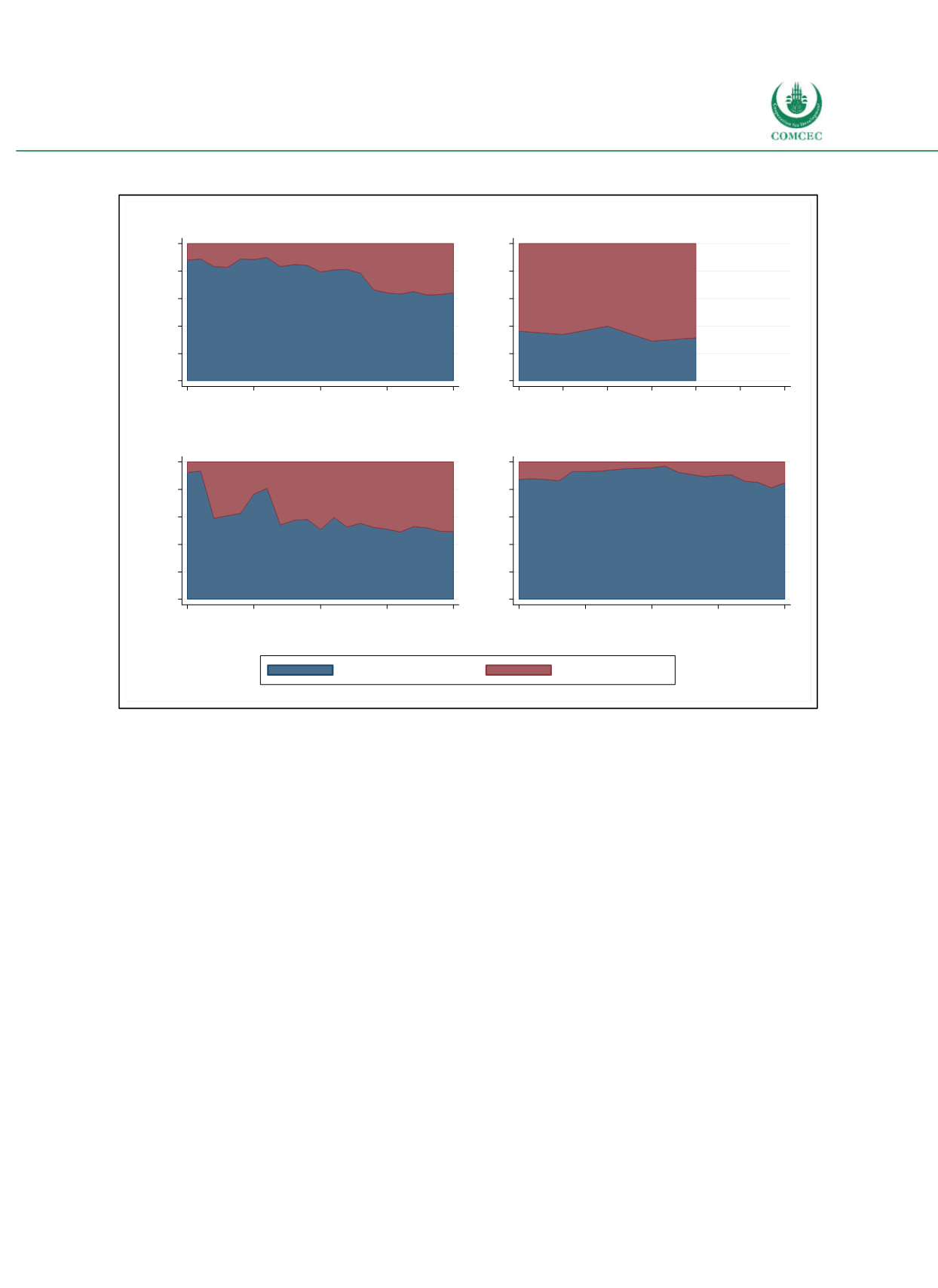

Figure 2-12: Currency Composition of Public Debt Worldwide

Sources: IMF and World Bank (2016), Quarterly Public Sector Debt database, calculations by the Ifo Institute.

Note: Due to missing data the graph for low income countries (top-right panel) covers a shorter time period only.

Which currencies dominate foreigndenominated public debt? The international role of the U.S.

Dollar is revealed in public debt contracts: the share of the U.S. Dollar in total foreigndenominated public debt has been rising over time and equals 59% in 2014 (see Figure 213).

The second most important currency is the Euro (13% in 2014), which took up the shares that

German Mark and French Franc occupied before its introduction. The share of the Japanese

Yen has been decreasing over time. It should be noted that there is an important role for

multiple currency arrangements, too. Overall, no significant difference in the currency

composition between middleand lowincome countries is observed. However, currency

denomination depends on the region (see Figure 214). While in Europe, Central Asia and

MENA the Euro is especially strong, Dollar loans are dominant in Latin America and the

Caribbean (89% in 2014). Asia has a larger share of the Yen at the expense of the Euro. In

general, apart from the global role of the Dollar, countries base loan contracts preferably on

the dominant currency of their region. This is reasonable, because trade revenues are often

denominated in this currency.

0

20

40

60

80

100

%

1995

2000

2005

2010

2015

Year

All income levels

0

20

40

60

80

100

%

2009 2010 2011 2012 2013 2014 2015

Year

Low income

0

20

40

60

80

100

%

1995

2000

2005

2010

2015

Year

Middle income

0

20

40

60

80

100

%

1995

2000

2005

2010

2015

Year

High income

Domestic currency

Foreign currency